Bookkeeping

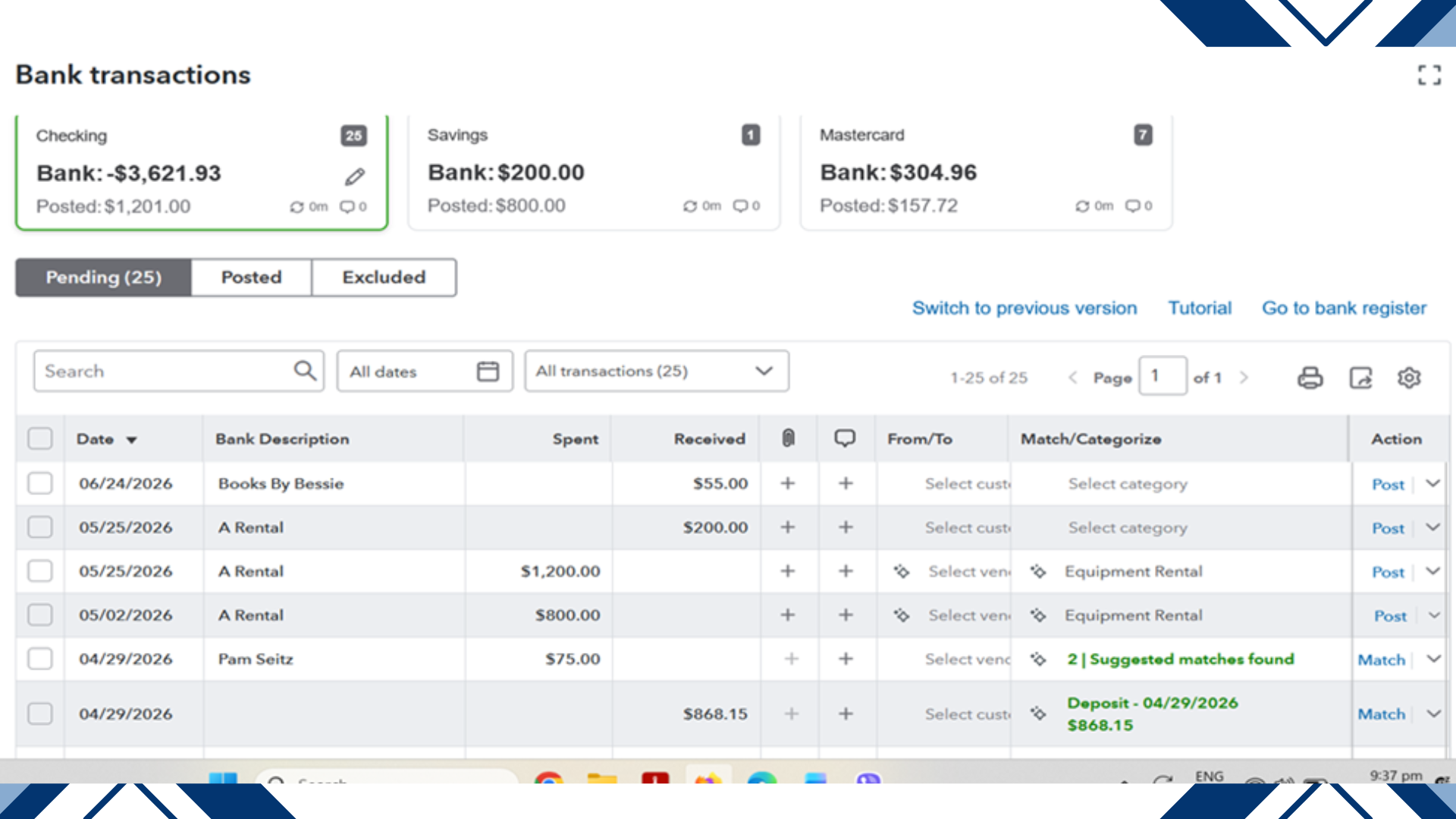

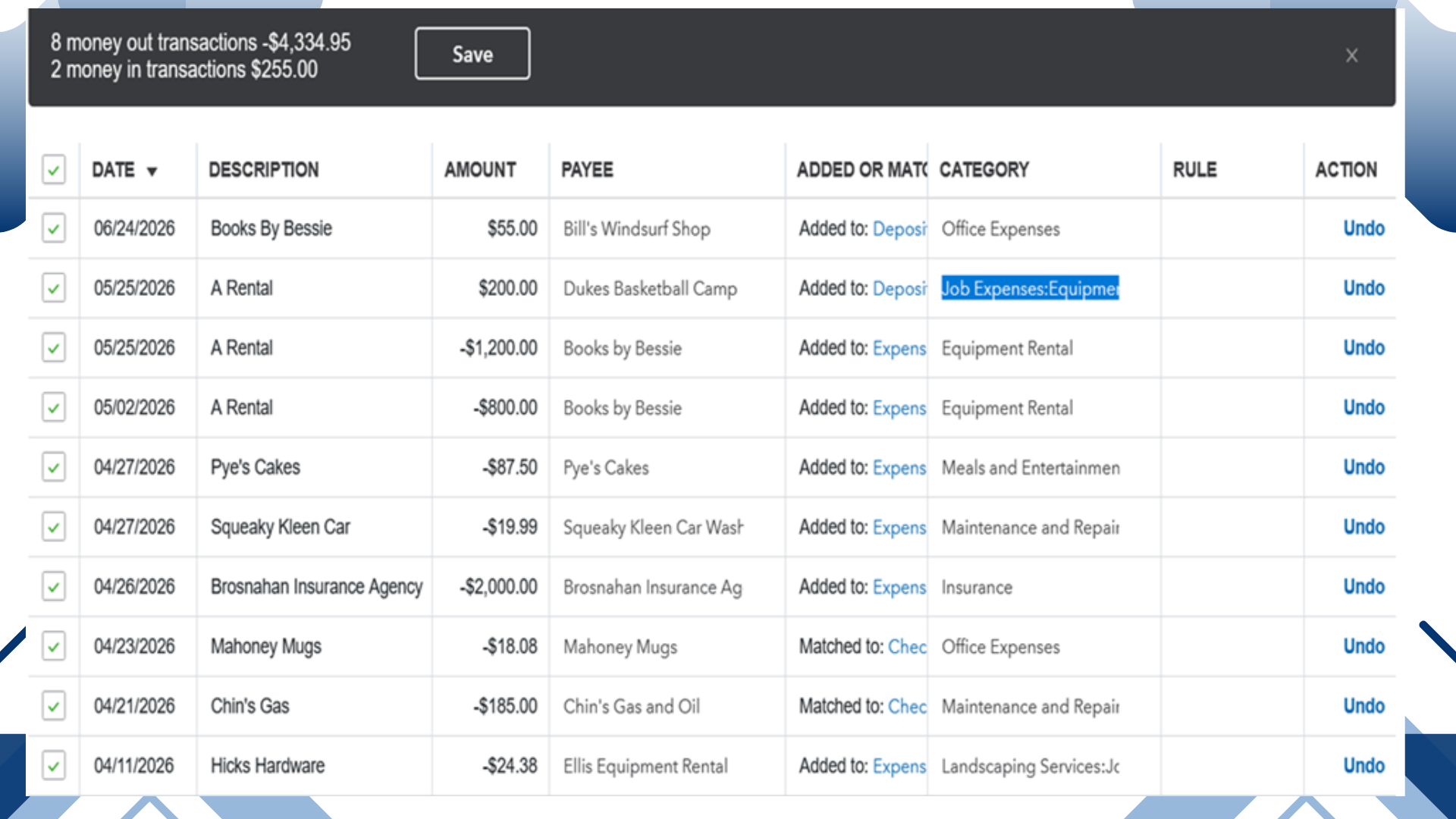

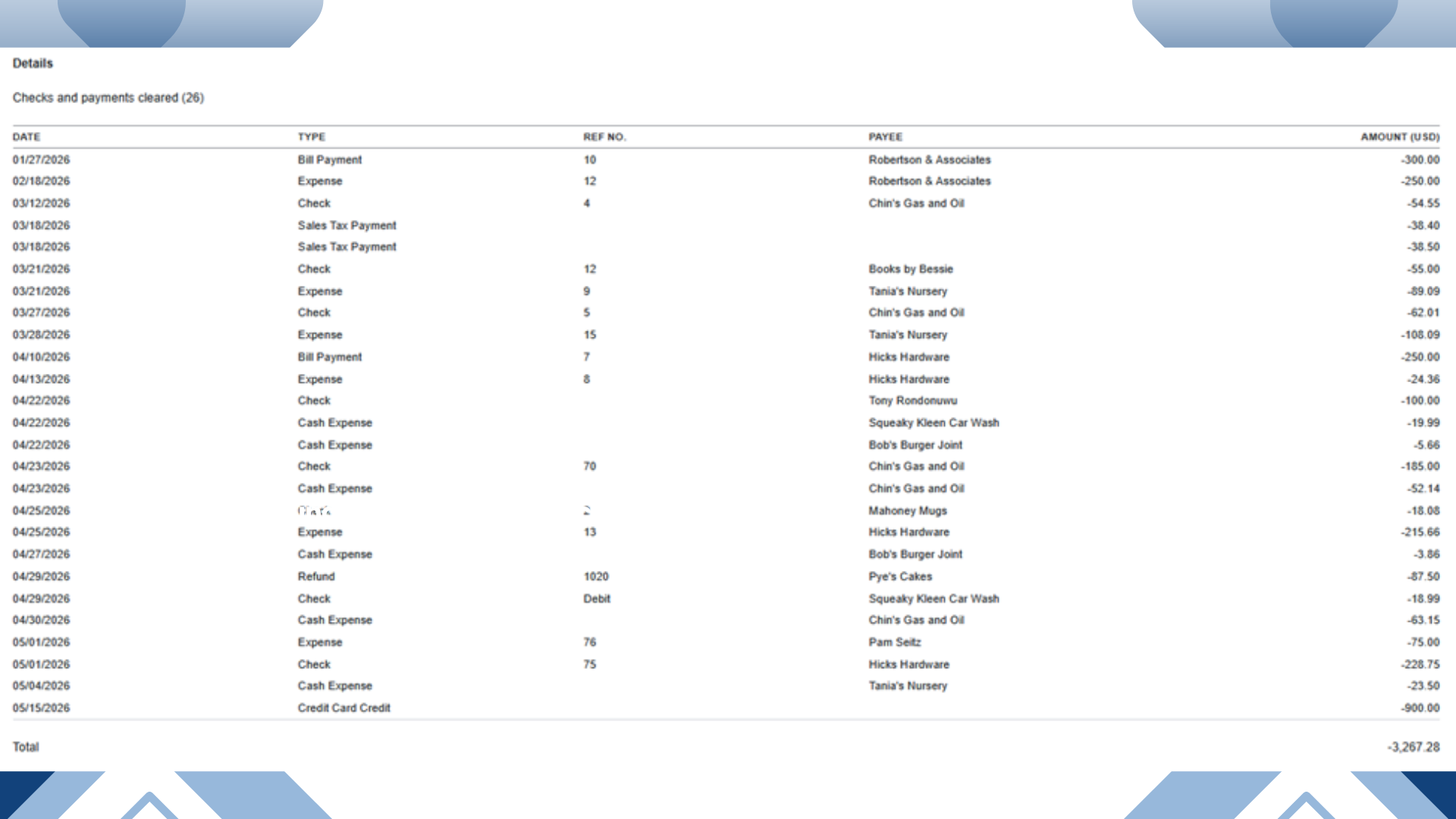

- Bank Transactions - refer to all the financial activities that flow between your business and its bank accounts. It makes it easier to track, categorize, and reconcile these movements so your records always match your actual bank statements.

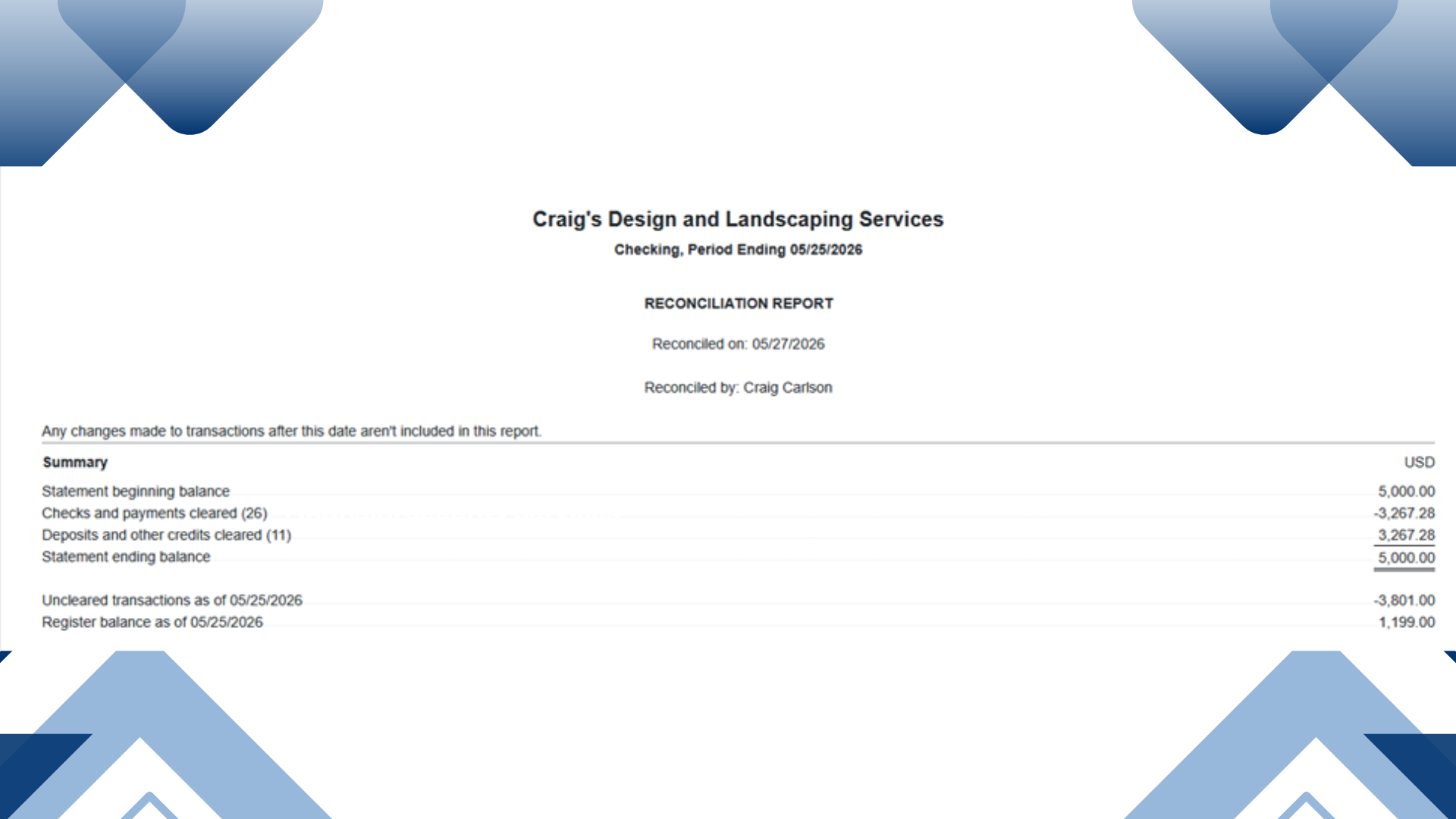

- Reconciliation - is the process of comparing your company’s financial records with your bank or credit card statements to ensure accuracy. It’s a critical step in bookkeeping because it confirms that the money recorded in QuickBooks matches the actual transactions processed by your bank.

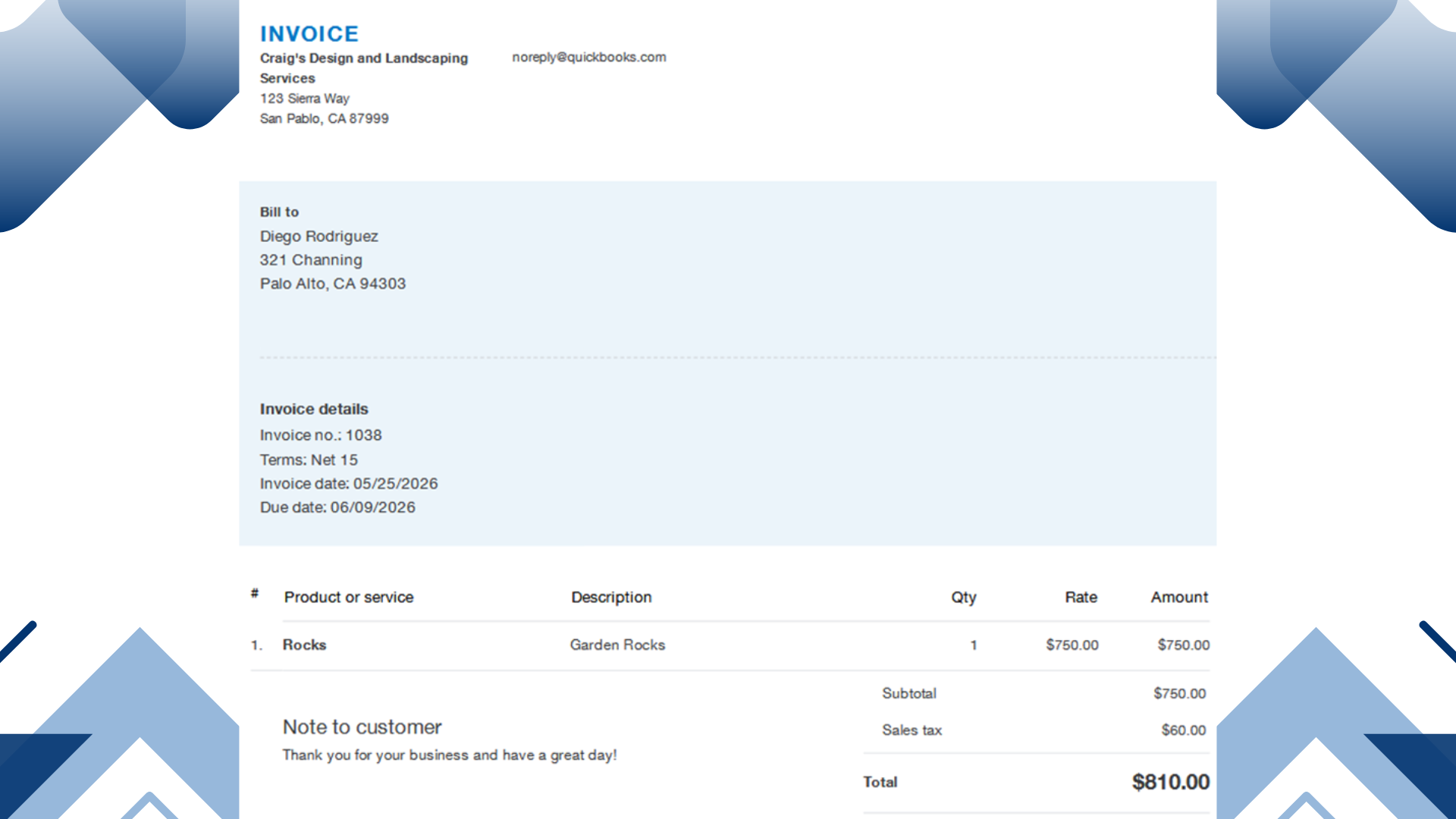

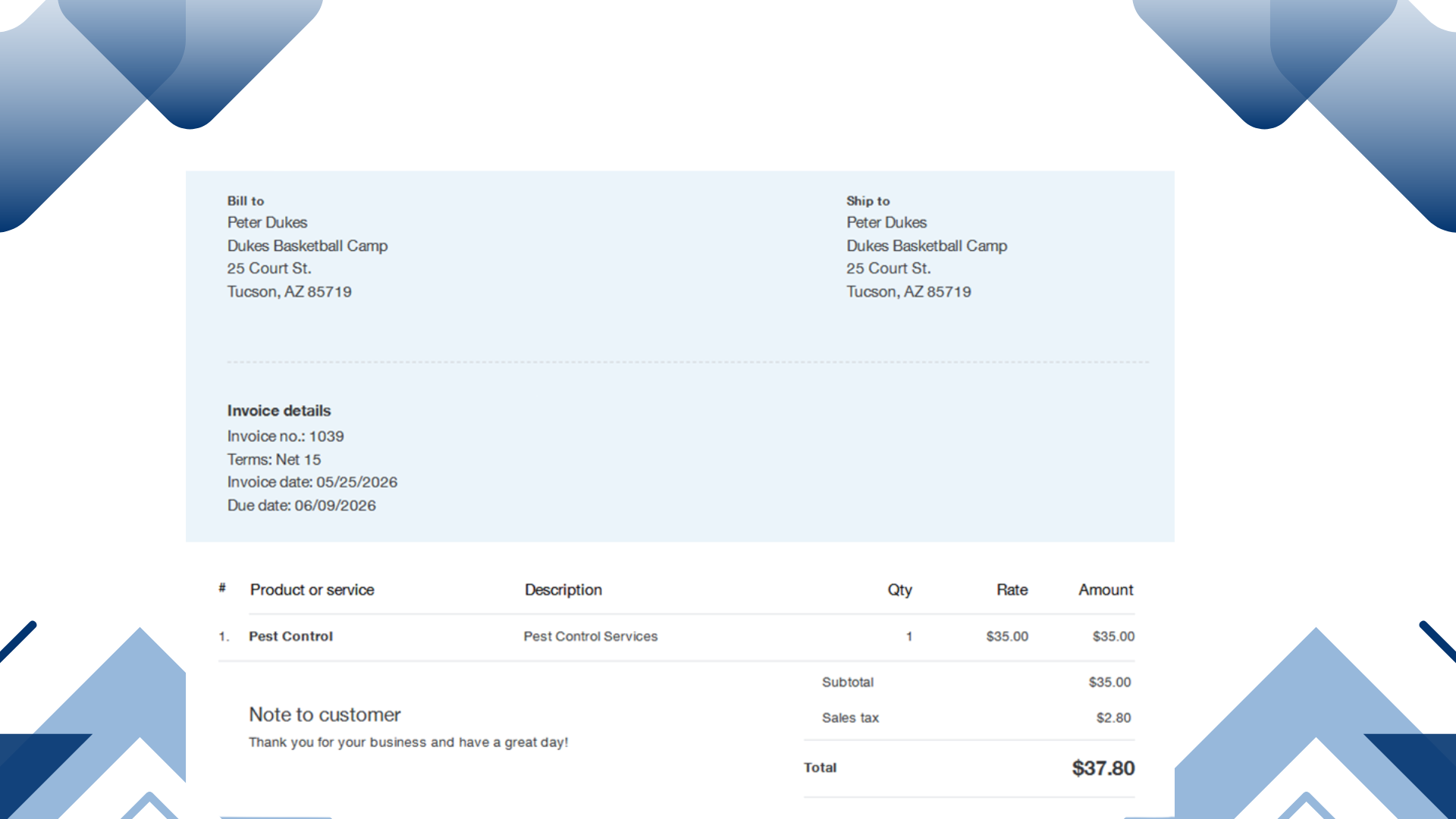

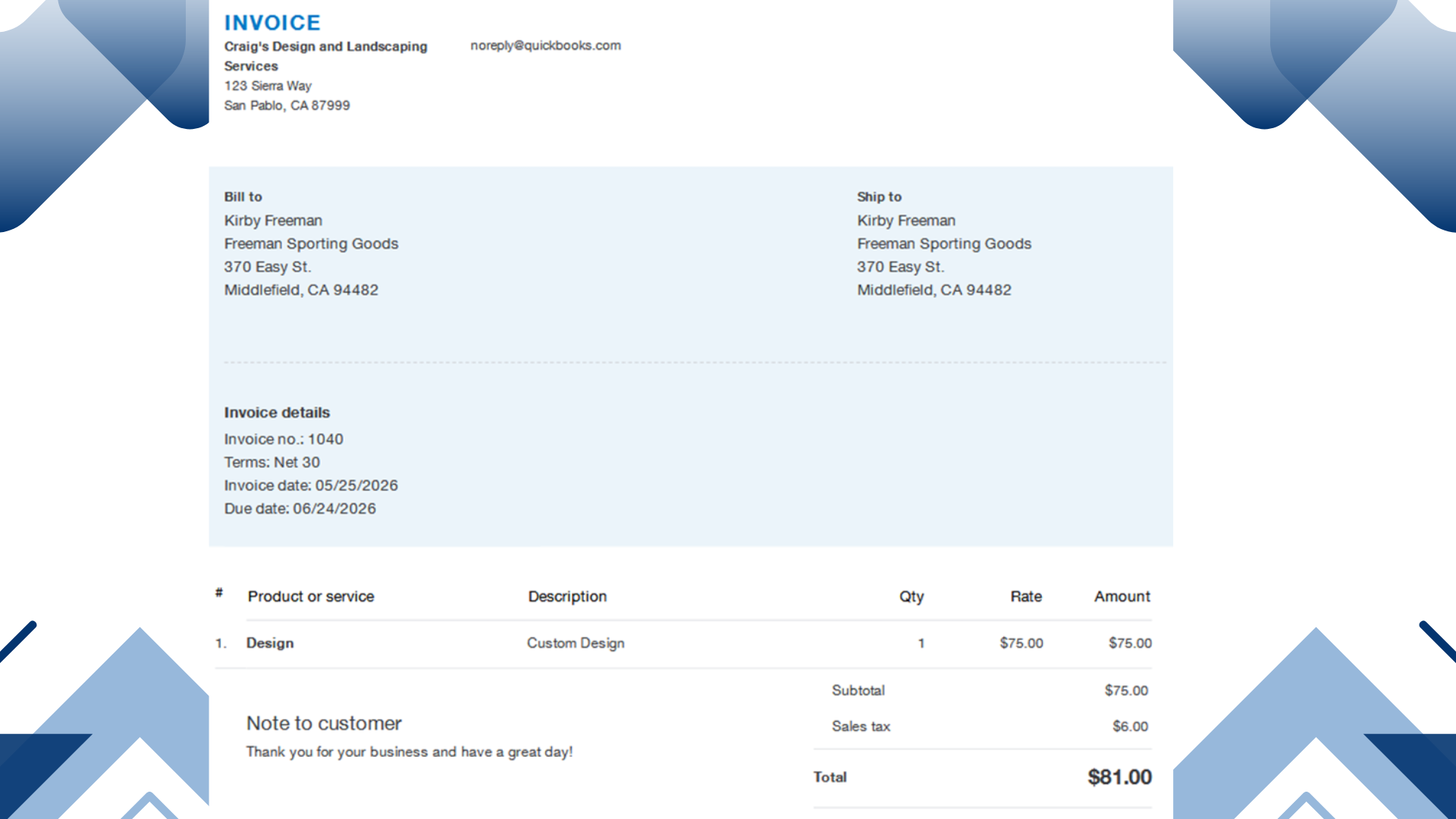

- Invoice - is a document you create and send to customers to request payment for products or services. It’s one of the most commonly used features because it helps track sales, customer balances, and accounts receivable.

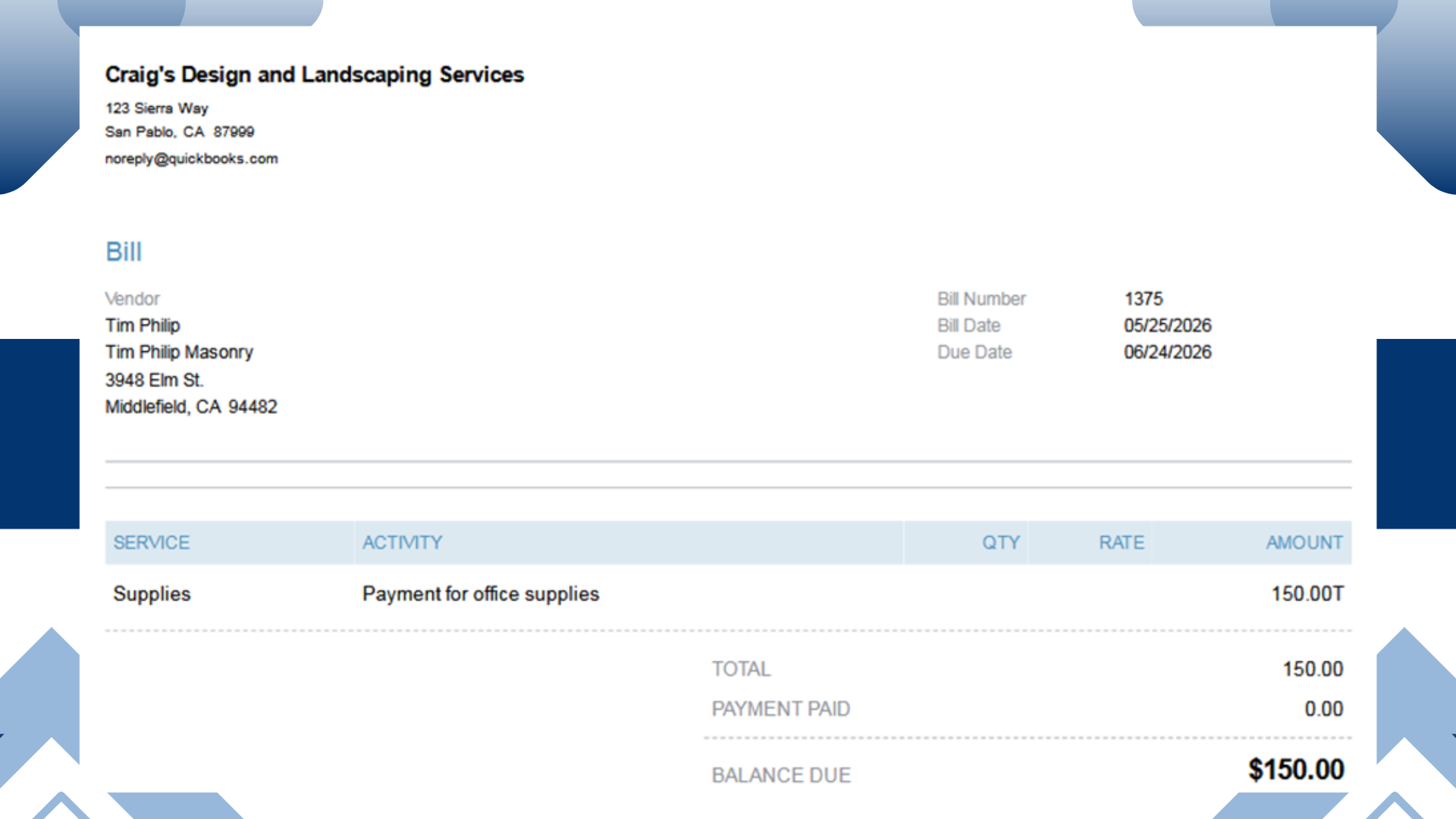

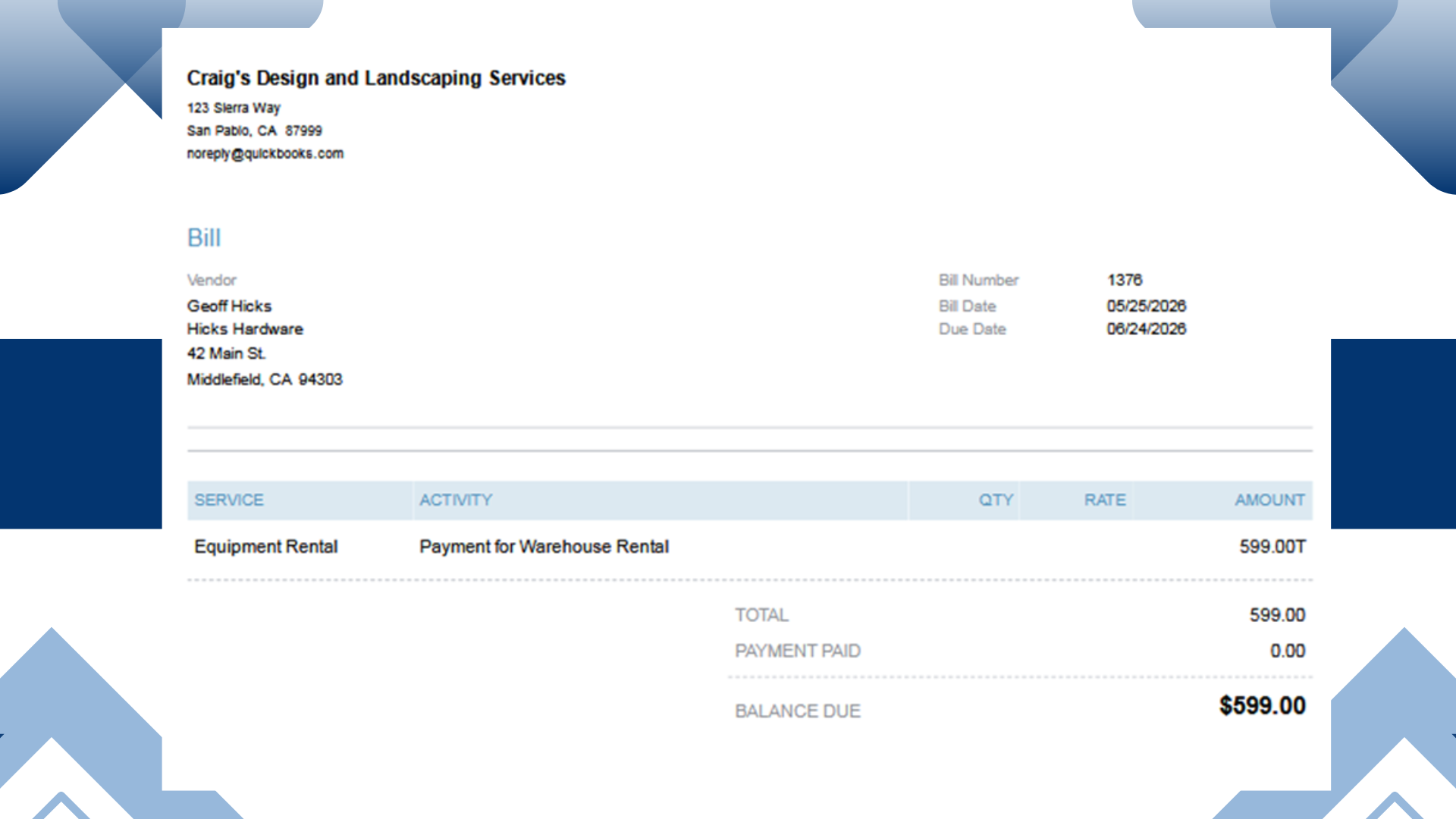

- Bill - is a record of money your business owes to a vendor or supplier. It’s part of the Accounts Payable (AP) process and helps you track expenses, due dates, and outstanding obligations until payment is made.

FINANCIAL REPORTS

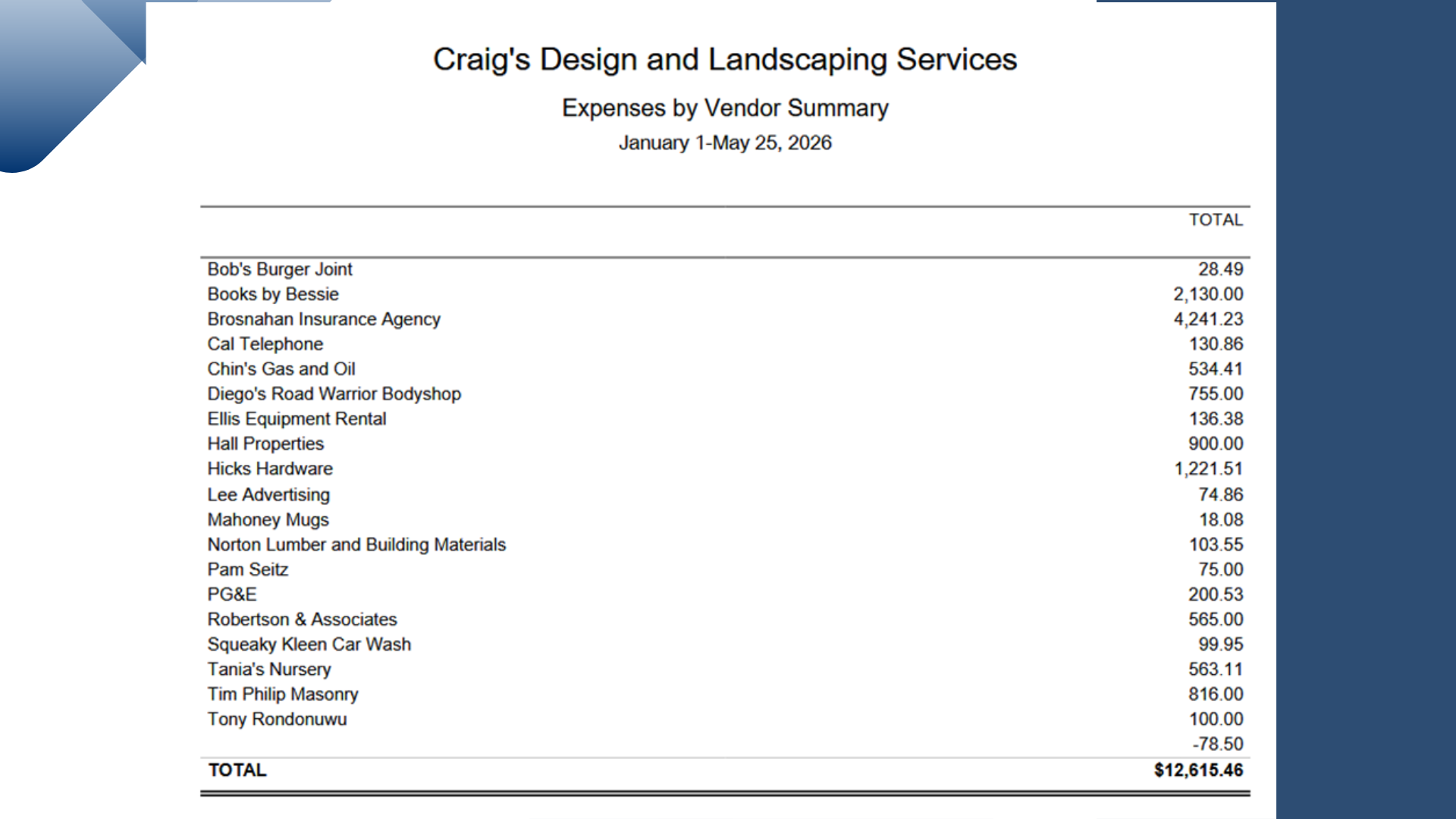

- Expenses by Vendor Summary -is a report that shows how much money your business has spent with each vendor over a selected period. It’s a powerful tool for monitoring costs, managing vendor relationships, and keeping track of accounts payable.

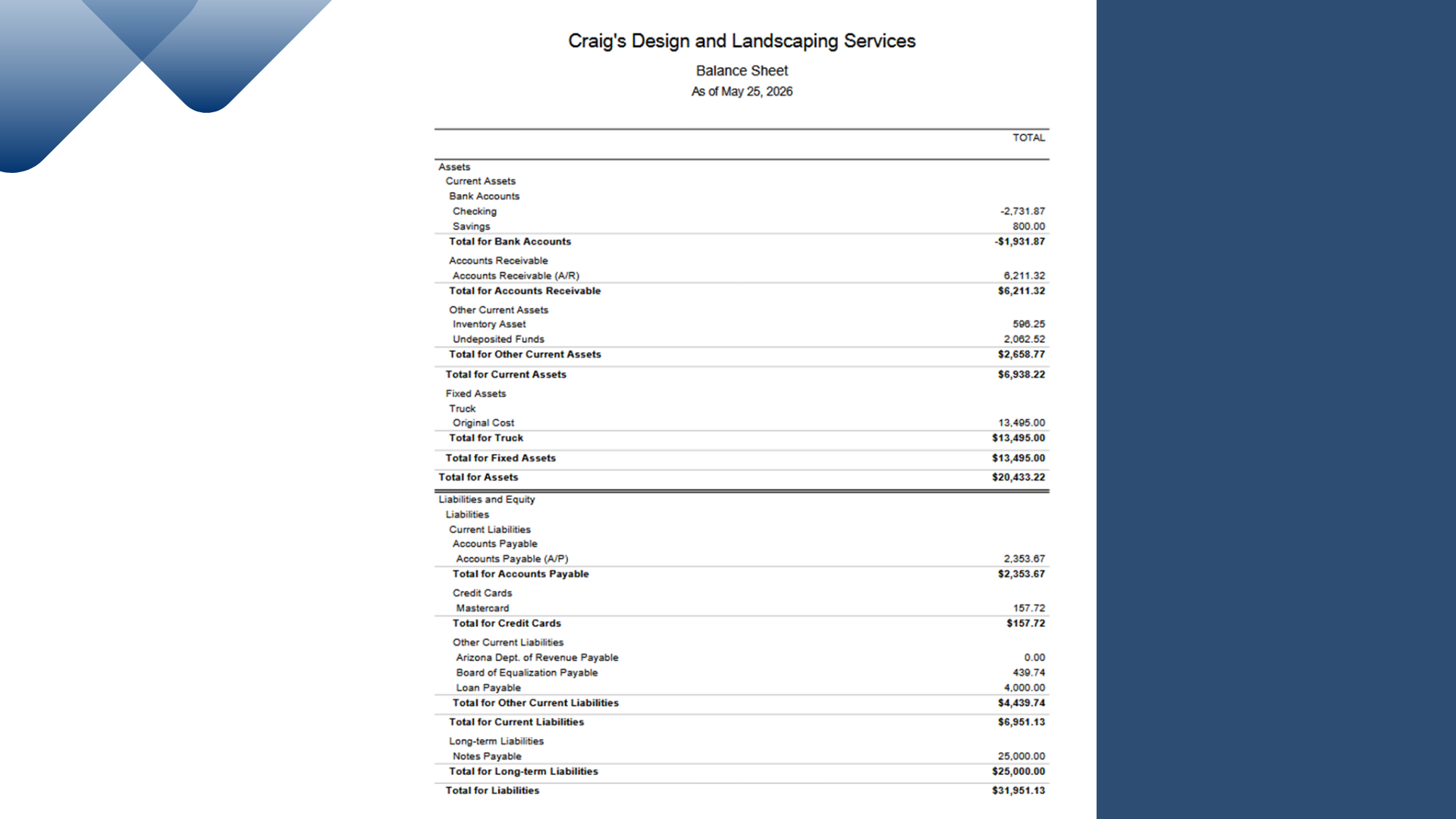

- Balance Sheet - is one of the core financial statements that shows a company’s financial position at a specific point in time. It’s divided into three main sections:

Assets – What the company owns

Current Assets: cash, accounts receivable, inventory

Fixed Assets: property, equipment, vehicles

Liabilities – What the company owes

Current Liabilities: accounts payable, short‑term loans, accrued expenses

Long‑Term Liabilities: mortgages, bonds payable, long‑term debt

Equity – Owner’s stake in the business

Capital contributions

Retained earnings (profits kept in the business)

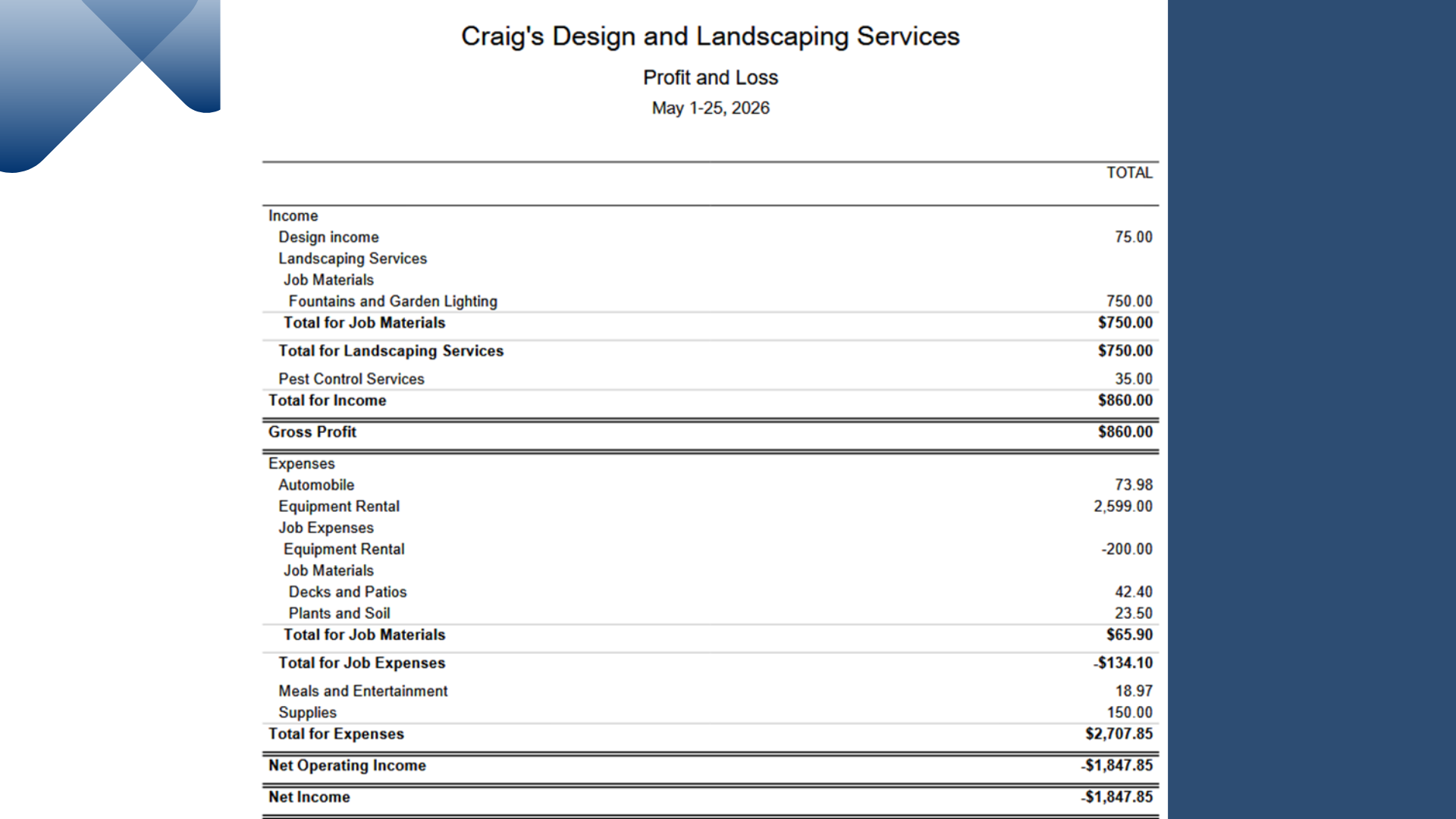

- Profit and Loss (P&L) Statement— also called the Income Statement — is a financial report that shows your company’s revenues, expenses, and net income (profit or loss) over a specific period of time. It’s one of the most important reports for understanding business performance.

What the Profit & Loss Report Shows

Income (Revenue) – Sales from products or services.

Cost of Goods Sold (COGS) – Direct costs of producing goods or services.

Operating Expenses – Overheads like rent, utilities, payroll, and supplies.

Net Profit or Loss – The bottom line after subtracting expenses from income.

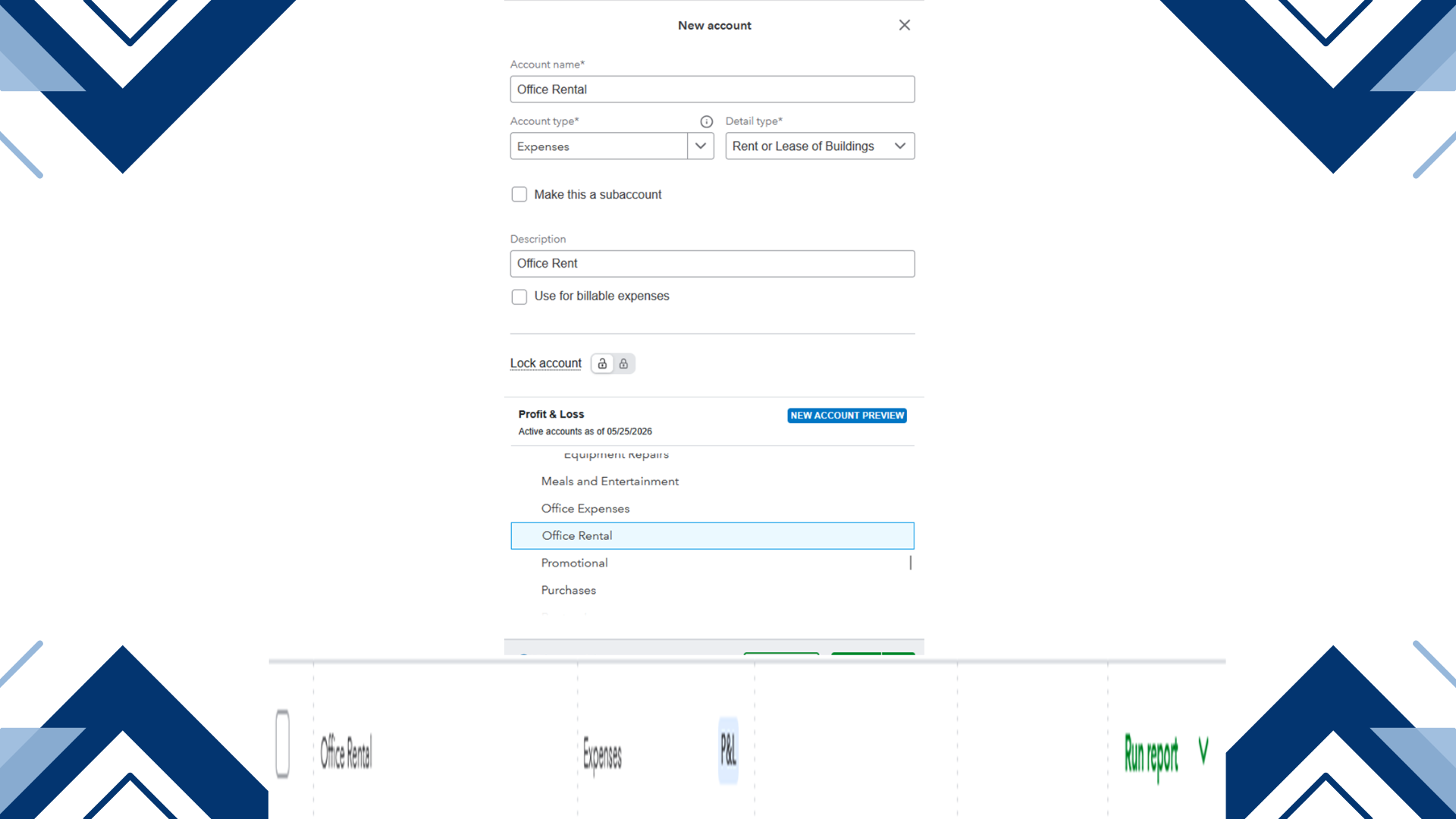

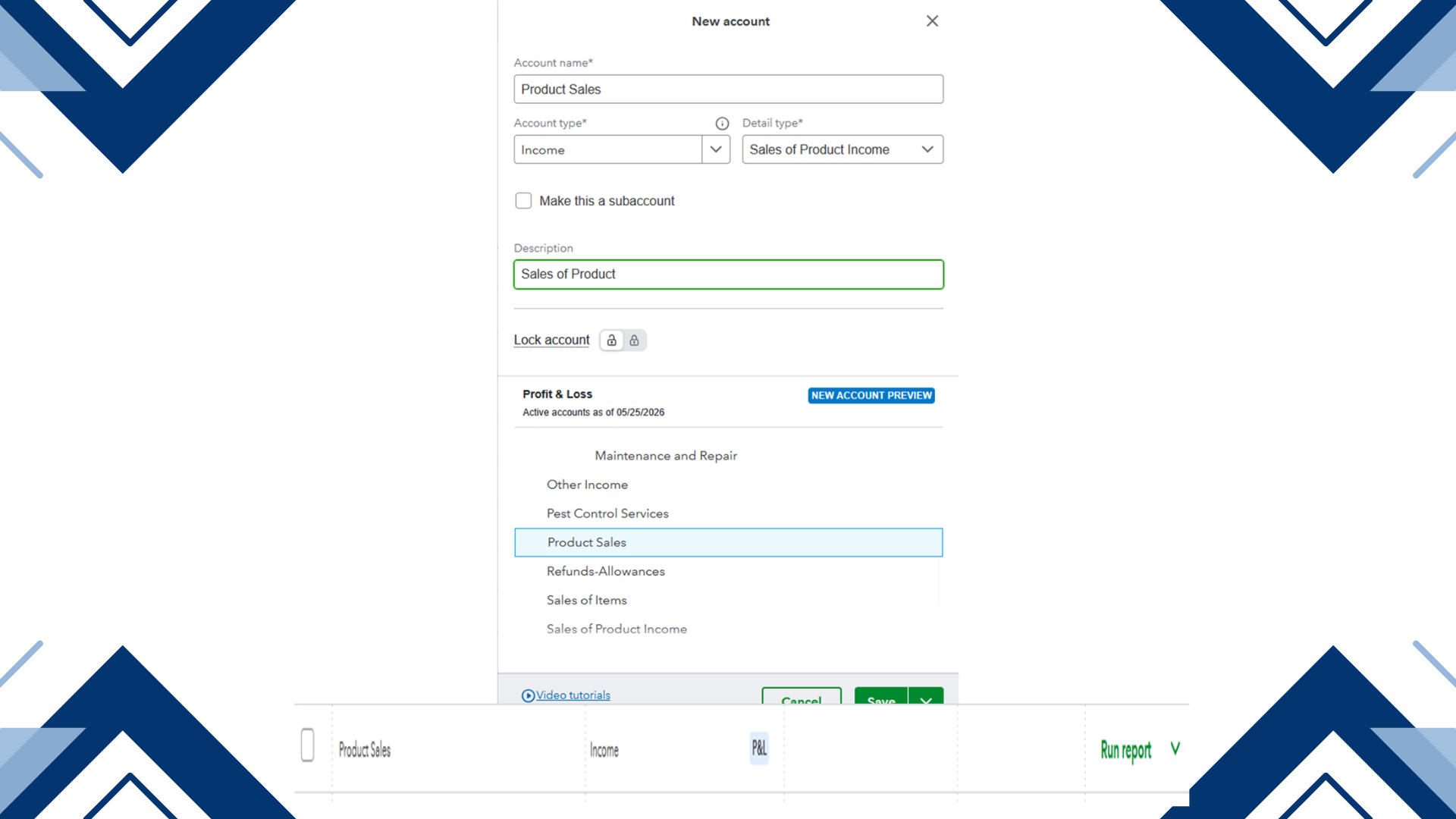

- Chart of Accounts (COA) is the backbone of your accounting system. It’s essentially a list of all the accounts you use to categorize transactions, giving structure to your financial data and making reports accurate.

What the Chart of Accounts Includes

Assets – Cash, accounts receivable, inventory, equipment.

Liabilities – Accounts payable, loans, credit cards.

Equity – Owner’s capital, retained earnings.

Income – Sales revenue, service income.

Expenses – Rent, utilities, payroll, supplies.

As a Bookkeeping Virtual Assistant, I provide accurate financial record‑keeping, organized reporting, and reliable support for business operations. With expertise in managing invoices, expenses, reconciliations, and spreadsheets, I ensure that financial data is precise, up‑to‑date, and easy to analyze. My commitment to confidentiality, efficiency, and attention to detail makes me a trusted partner in helping businesses maintain clear accounts and achieve financial stability.